The U.S. housing market is projected to continue its positive pace in 2018 as recent ficscal policy changes flow through the system. However, affordability for first-time homebuyers will remain challenging as prices rise across the country, mortgage rates inch higher and fewer entry-level homes come onto the market.

The U.S. housing market is projected to continue its positive pace in 2018 as recent ficscal policy changes flow through the system. However, affordability for first-time homebuyers will remain challenging as prices rise across the country, mortgage rates inch higher and fewer entry-level homes come onto the market.

The consensus among economists is that long-term mortgage rates will rise slowly next year in response to actions by the Federal Reserve to increase short-term interest rates. While the 30-year mortgage rate is not expected to climb above 5 percent, an increase of that size will hurt affordability for homebuyers, especially first-time purchasers. For example, a homebuyer obtaining a $150,000 mortgage at 4 percent (the average for a 30-year mortgage, as reported by Freddie Mac) paid approximately $716 monthly in principal and interest in 2017. If the rate were to climb to 5 percent, as some economists think it could by December 2018, the payment would jump to $805.

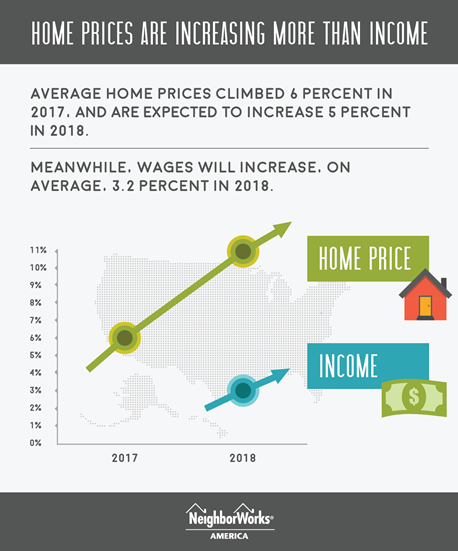

Meanwhile, home prices are rising as well, creating a pincer-like effect for homebuyers. Analysts at Corelogic reported that average home prices climbed 6 percent in 2017, with Freddie Mac pegging the increase at 6.7 percent. The two companies predict a 2018 increase of 5 percent and 5.7 percent, respectively.

Mortgage and home-price forecasts wouldn’t be so onerous if income growth kept pace. However, few, if any, economists expect income to keep up with home prices. The Economic Research Institute recently surveyed employers, and the consensus is that wages will increase, on average, only 3.2 percent in 2018—not enough to offset home price growth.

These factors are leading homebuyers, especially younger people, to be pessimistic about their homebuying options. The NeighborWorks 2017 America at Home Survey found that nearly half (49 percent) of millennials said they are more likely to rent a home as their next housing choice, instead of purchasing. That’s because rent is too high for them to save enough for a down payment to buy a home in their preferred community. Specifically, 63 percent of millennials in the NeighborWorks survey said “rent is too high to be able to save for a future home.”

Compounding these concerns is a severe lack of supply of affordable homes for purchase. We think a relatively low supply of new, entry-level-priced homes (below $200,000) for sale will continue in 2018. According to the U.S. Commerce Department, 72,000 homes were sold in the first 10 months of 2017 at a sales price below $199,000. That compares to 291,000 homes priced between $201,000 and $399,000.

Now for the bright side: We expect to see nonprofit housing organizations to conduct more outreach to consumers who want to purchase homes. NeighborWorks organizations already are expanding their delivery of homebuyer education, both in-person and online. Homebuyer education introduces consumers to mortgage products that can help overcome some of the obstacles to homeownership, including issues related to down payment and credit.

NeighborWorks America also projects that first and second mortgage-origination lending will grow 22 percent among its members by the end of 2017, providing the momentum to continue strong volume next year.

12/18/2017